Are LNG exports good for the USA?

Let's get the policy right to avoid future natural gas price spikes.

Make someone’s day: Gift a subscription to your friends and family!

As most of my readers know, I am obsessed with energy, and rightfully so. Energy is essential for life; Energy is essential for complex societies; Energy is essential for human material progress. And for the last two centuries, the overwhelming majority of that energy has come from fossil fuels - coal, crude oil, and natural gas. I seriously doubt that will change within the next 20 years.

In this article, I will focus on a specific form of natural gas called Liquified Natural Gas (LNG). Natural gas is an incredibly flexible source of energy. No other energy source offers so many uses and so many advantages. Because natural gas is… well.. a gas, so it has one big disadvantage: it is very hard to transport across oceans (at least until recently).

Crude oil and uranium are both easy to transport across oceans. This creates truly global markets for those two energy sources. Natural gas is largely transported via specialize pipelines.

{kind=link}

Natural gas pipelines are a very cost-effective means of energy distribution across land. Natural gas pipelines can transport far greater volumes of energy (10-25 GW) than electric power lines (2-3 GW). Energy losses during transmission are also far lower than for electricity (Smil 2015).

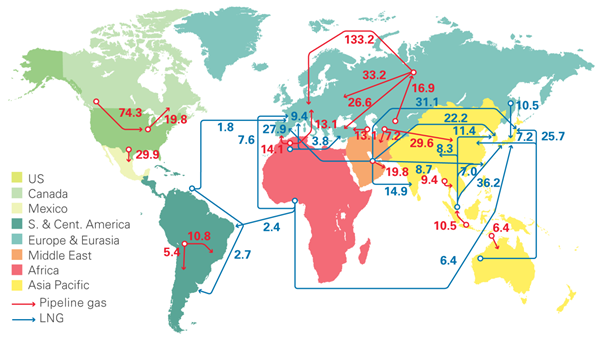

Unfortunately, natural gas pipelines do not work so well under oceans. This effectively means that natural gas markets are chopped up into many regional markets. Each regional market is delineated by a web of pipelines and each network has its own separate price structure that is dictated by the supply and demand within the network.

{kind=link}

So while the price of crude oil is roughly the same in the USA, Japan, Russia, Europe, Africa, and Asia, the prices of natural gas are often very different. Any nation that wants greater access to the world crude oil market just needs to construct a port (assuming they have a coastline). Natural gas pipelines have to cross national borders and potentially span very politically unstable regions (I am looking at your Middle East!).

So if we have a way to turn natural gas into a liquid, then we can potentially create global natural gas markets like we already have for crude oil.

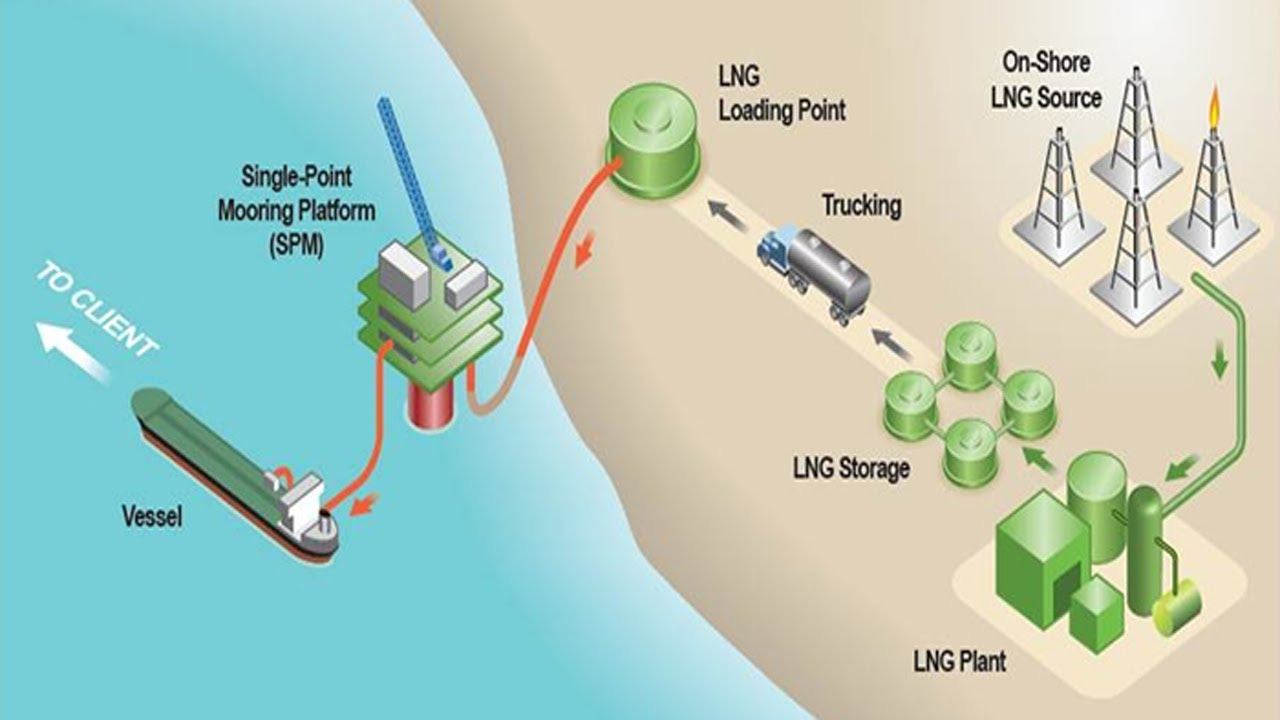

Enter LNG. LNG is natural gas that has been cooled down to −162 °C (−260 °F) so that it becomes a liquid.

{kind=link}

The liquid can then be pumped onto a ship that looks alot like a crude oil tanker with pressurized containers.

{kind=link}

The oil tankers can then transport the LNG across the ocean to any specialized LNG port. The LNG is then thawed so it becomes a gas again, and then the natural gas is pumped into the existing natural gas pipeline network. Now it is just like any other natural gas.

Like magic, natural gas is now a global commodity that can be transported between existing natural gas pipeline networks instead of just within them. There is just a few catches:

LNG is much more expensive the traditional natural gas (at least under existing technology).

LNG plants are very expensive and time-consuming to construct, so the private industry needs to be confident that the demand and price will be high enough in the future to justify the construction cost. These plants also require government approval.

Connecting regions with low natural gas prices (like North America) to regions with high natural gas prices (like Europe) raises the price of natural gas in the region with lower prices.

Once natural gas distributors have access to premium overseas prices, they prefer to export LNG, which potentially causes shortages in the domestic market. Without increased natural gas production, domestic prices spike and consumers are outraged by far higher gas bills for no apparent reason.

See also my other posts on Energy:

You might also enjoy reading my “From Poverty to Progress” book series:

Russia introduces Europe to reality

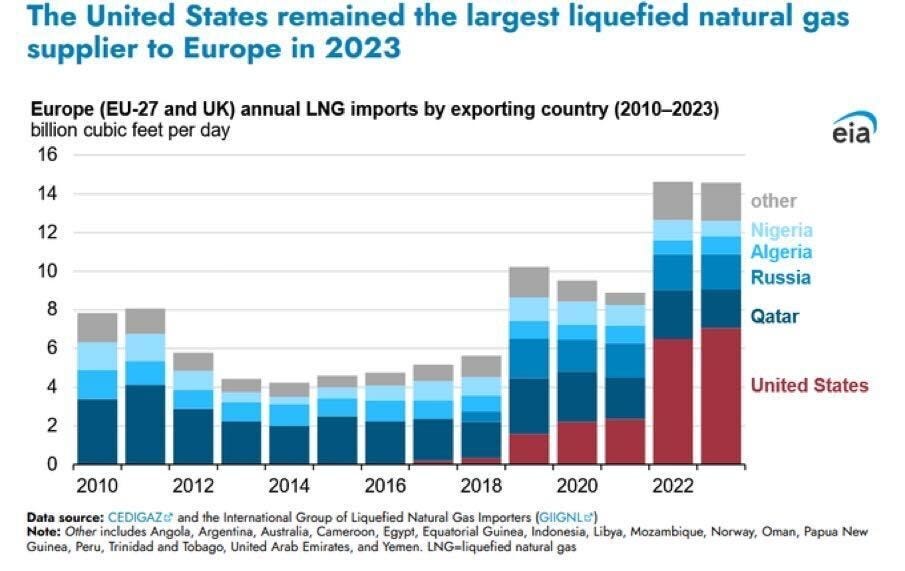

This is exactly what happened in 2022 after Russia invaded Ukraine and then in retaliation Europe stopped importing Russian natural gas. Western Europe’s Green energy policies of the last generation made Europe very dependent on Russian natural gas. When that supply was suddenly removed, European natural gas prices spiked. This could have devasted the Western European economies, but fortunately, the United States had spare LNG capacity. The USA (along with Norway) rushed in to fill the gap with American LNG and Norwegian conventional gas.

This in turn caused a price spike within the American natural gas network.

Fortunately for the United States and Europe, the American shale gas industry was able to react quickly and increase production. Within less than two years, prices were back to their previous lows.

By the way, this ability to rapidly increase natural gas production due to sudden swings in supply and demand is one of the great advantages of shale gas production compared to conventional natural gas production. Unlike conventional gas fields, shale producers can cap individual sub-sections of drilling pads for later extraction. This means that shale gas producers can drill in bulk to save cost, but then extract the gas only when the supply is necessary.

Just-in-time natural gas production!

Of course, all of this is dependent upon excess capacity of LNG ports and LNG ships being available. Natural gas bottlenecks can happen:

at the well or

at the LNG port, or

by a limited number of LNG ships.

Unfortunately, the Biden administration tried to ban the construction of new LNG ports, extensively for climate reasons. Fortunately, the Trump administration is almost guaranteed to do the opposite. This will likely substantially increase LNG port capacity in the next four years.

What about future price spikes in USA?

In general, I believe that exporting LNG to our allies is a good policy. Without American help, our European allies might have caved into Russian demands, and the NATO alliance might have fragmented.

So while it was much smaller in scale, the 2022 LNG exports was similar to the USA bailing out Europe in World War I, World War II, and the Cold War. It was a necessary action.

This still confronts the United States with the possibility that shortages in natural gas overseas, particularly Europe, will cause price spikes in the United States as producers rush to take advantage of the higher overseas prices.

This is very much like the current situation in Europe where German Green energy policies and the decommissioning of domestic nuclear plants have caused electricity prices to spike all over Europe. These huge electricity price spikes is threatening to destroy the European electrical grid as other nations do not want to bear the burden for Germany’s bad energy choices.

Unfortunately, all it takes is for one nation having stupid energy policies for all other nations in their network to suffer the consequences.

So I suggest the following:

President Trump agrees to the construction of new LNG ports in the US. If private companies believe that they can make a profit, we should allow them to do so.

But in return Trump should establish an LNG international export “price ceiling” of $5 per million BTU. When domestic Henry Hub gas prices go above that price, LNG ports may not export overseas. This price ceiling will have no effect on domestic distribution or production, nor will it effect the price of LNG sold to other nations. The price ceiling effectively ensures that American consumers will not be punished for overseas shortages.

The $5 per million BTU is above the typical natural gas price for the last 20 years, but below the price spikes of 2014 and 2022 (Russian invasion), so it will only take effect during emergencies. In most years, the ceiling will have no effect.To export LNG to another nation, the importing nation must allow American shale gas companies to explore and drill within potential conventional and shale gas fields on their territory. In other words, nations cannot ban domestic natural gas exploration and production, while forcing American consumers to pay higher prices caused by their ban.

Unfortunately, we have many nations, particularly in Europe, that refuse to allow domestic shale gas exploration and production, while importing natural gas from other nations. This is exactly what caused the 2022 natural gas price spike.

If you want American natural gas, you cannot ban domestic natural gas.

Let’s globalize the Shale gas revolution

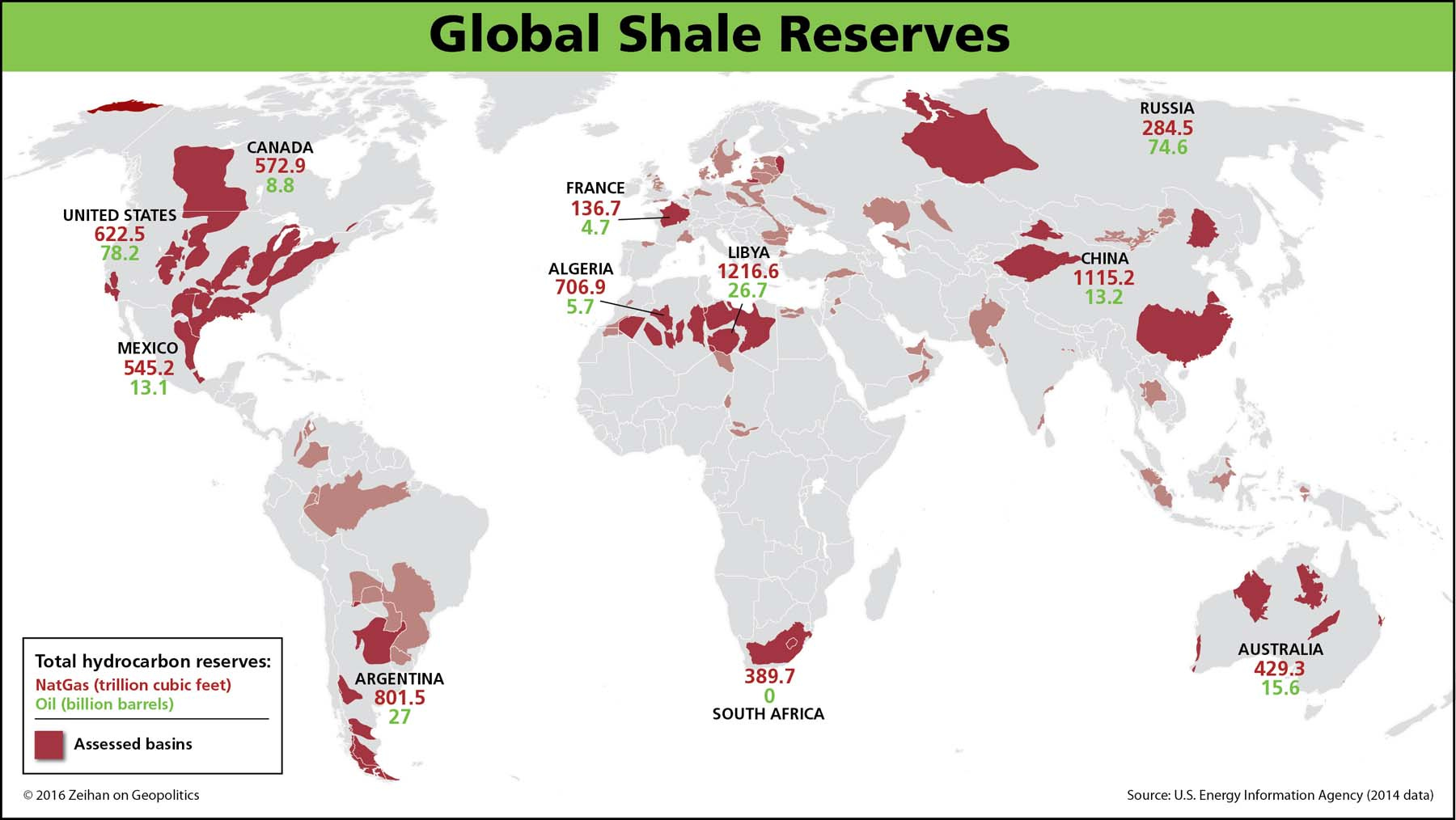

As of today, shale gas is almost exclusively an American phenomenon. This is not primarily due to geology. Contrary to what many think shale gas fields are spread widely across the globe.

The reason is government policy. Other nations lack of technology, skills, and capital to explore and drill within their domestic shale gas field, and government prohibit the practices. So they cannot learn from the Americans.

If the Shale Revolution spreads to the rest of the world, it would be one of the most important energy revolutions in world history. It would complete the Third Energy Transition. The only force stopping this revolution are Green policies that make the exploitation of shale gas illegal, or at least very expensive.

Shale gas is a revolutionary energy source because it is so widespread globally. Substantial shale gas fields are located in every region, and in seven of the ten most populous nations:

India (the largest population in the world)

China (second most populous)

USA (third most populous)

Indonesia (fourth most populous)

Pakistan (fifth)

Russia (ninth)

Mexico (tenth)

In addition to the above, substantial shale gas fields are located in the following economically important nations:

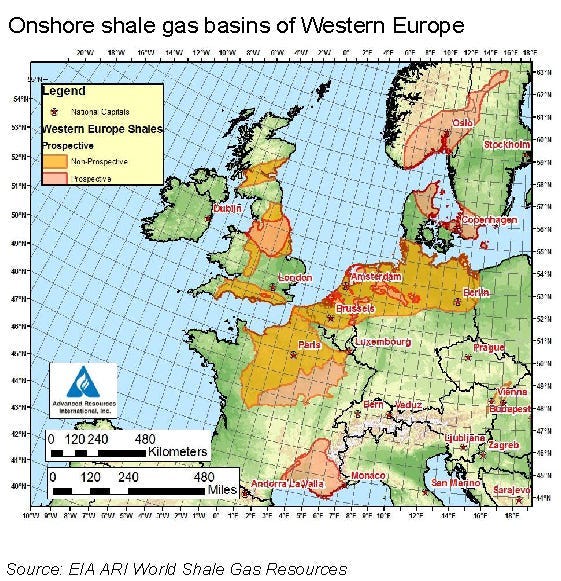

In Europe, the United Kingdom, France, Germany, Poland, Romania, and Ukraine.

And this is just the beginning. Based on past performance, it is very likely that new fields will be discovered and the technology to exploit them will get more and more cost-effective.

The known shale deposits are already greater than all conventional deposits in Saudi Arabia and Russia combined. The main problem with shale fields is that each has individual characteristics that require high levels of expertise to locate and extract oil and gas. Currently, only American companies have that expertise (Zeihan 2016).

So the third clause in my proposal will encourage foreign nations to join the Shale gas revolution and dramatically increase domestic natural gas production. This will enable far more of the world to enjoy the benefits of affordable and abundant natural gas, while transitioning from coal to far more environmentally-friendly natural gas.

That would be a:

A Win for energy security

A Win for military security

A Win for economic growth

A Win for the natural environment

See also my other posts on Energy:

You might also enjoy reading my “From Poverty to Progress” book series:

Here are some more great energy-related Substack columns that you might be interested in:

The price cap seems unnecessary and likely to backfire. Aren't those incentives to expand development in the US?

I still wonder if the entire NG energy infrastructure was a mistake from the beginning. Especially now where we see this need for LNG commerce to sustain it.

The alternative strategy would have been Methanol, which can be piped at much higher energy densities than NG, and transported by rail or ship at similar energy densities to LNG but without having to refrigerate it down to -260 degF. And the methanol being far easier to store than NG or LNG, while being easy to use in existing ICE vehicles, ship or rail. Burns at higher efficiency and just as clean as NG in gas turbines or ICEngines. Particularly good for local storage at peaking or backup NG power plants. Methanol being as easy to store as diesel but much less costly and spills are environmentally benign.

And methanol can easily be made from NG, coal or any biomass. In fact it is cheaper to convert NG to methanol at source and transmit by pipeline to a power plant, rather than by a CNG pipeline if the distance is larger than 5000kms.

At least in areas that have no developed NG infrastructure, such as a lot of Africa, it would be better to develop methanol infrastructure. Where locally produced methanol can still be delivered by truck, ship or rail until pipeline infrastructure can be developed.